- The Running Signal

- Posts

- Hard Resets

I've spent almost two decades watching freight markets absorb shocks. Demand collapses, capacity crunches, the slow bleed of a four-year downcycle that wrung out carriers, brokers, and shippers alike. Through the latest downturn, the industry saw a net loss of over 20,000 interstate carriers. Small businesses, mostly. The kind running three trucks and living on thin margin. The losses of larger operations come from places that can least afford them. You develop a feel for cycles not just from the data but from the psychology underneath them. How long people hold positions they know are wrong because changing them feels worse than staying put. That psychology is what I want to talk about today, because I'm seeing it everywhere right now, and not just in freight. And it's happened to me too.

The upside looked nearer the clouds going into 2026. I was sure we wouldn't see enough momentum until the end of the quarter at least. But the blip turned into a bump and now we're into months straight of rejection rates above 10% nationally. Flatbed has broken the door down. I've put my bull hat back on. The data earned it. Two straight months of manufacturing expansion. Backlogs at their highest since 2022. Rail and truckload both being fed. The heartland joined the recovery. Van rejections climbed from roughly 5% in October to the teens by February and have held. The air pocket closed. Rates aren't rising because of hype. They're resetting because volume, capacity, and fuel costs have all coalesced into a cost floor that carriers can no longer absorb. And will no longer absorb. That momentum was building from 2024 into 2025 until tariff uncertainty became the spoke in the wheel. Now we're waking up into a potential Groundhog's Day.

What I also know from nearly two decades of riding these cycles is that the freight market doesn't transition gradually. It jolts. On the way down, carriers hold rates longer than they should because giving ground feels worse than staying put, and then enough of them hit the wall simultaneously and the floor drops fast. On the way up, shippers hold out for gradual relief that never comes because capacity was hollowed out through years of cost-cutting and attrition. Small exits happen quietly at scale, but when a mid-size or regional carrier goes under it destabilizes entire lanes and sectors. Remaining capacity concentrates. Pricing moves faster than anyone modeled. The trade window opens and closes before most people realize it moved. Rejection rates don't drift from 5% to 15%. They snap there. That's the pattern I'm watching at a macro level right now, and it's why the current calm in equity markets feels less like stability and more like a held breath.

Duncan Weldon put it plainly this week: oil and energy market types are beginning to really freak out, while global macro types remain mostly calm, expecting this to blow over. Joe Weisenthal at Bloomberg called the current combination of signals the most uncomfortable since 2008, citing rising oil, softening jobs, Treasury volatility, and private credit showing stress, while being careful to say we're not on the doorstep of crisis. That carefulness is worth examining. It's not dishonesty. It's the rational posture of people who know that being right about a structural thesis at the wrong time is just as costly as being wrong. You can't trade on a thesis until the signal fires. So sophisticated actors who privately see the risk stay publicly measured. The repricing waits. And so does the damage.

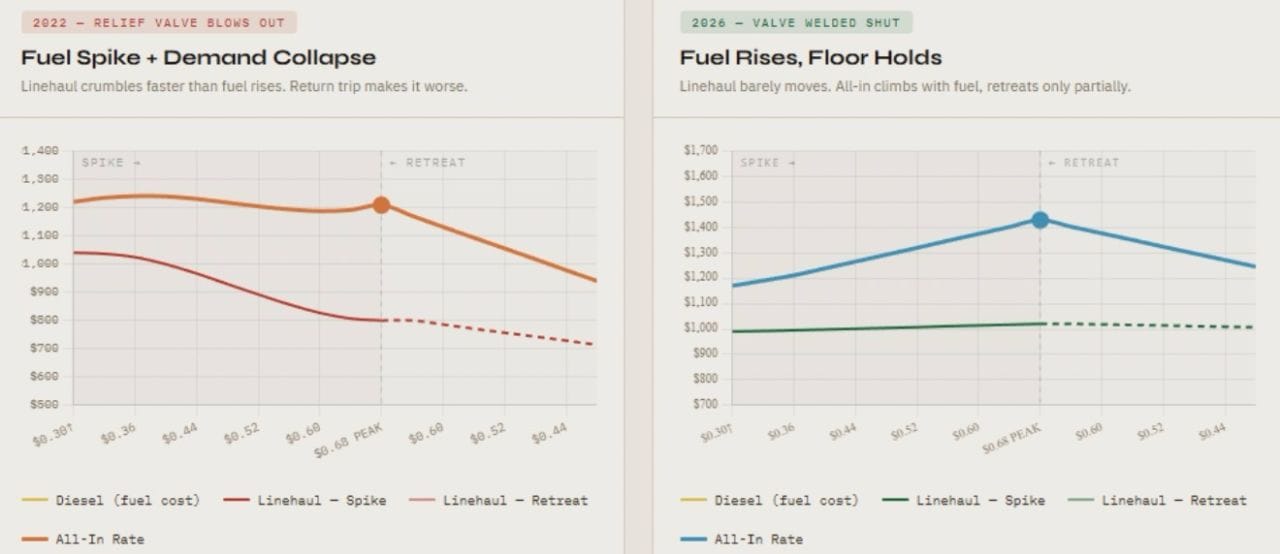

Shared by Patrick De Haan of GasBuddy

The oil number deserves specific attention because it just became impossible to ignore. The national average price of diesel recorded its largest single day increase ever this week, rising 22.3 cents per gallon, narrowly beating the previous record set in March 2022. That record was set when the market had a release valve: demand was collapsing, linehaul rates absorbed the pressure downward, and the fuel spike actually accelerated the crash. The market is different now. Linehaul has a floor. Capacity is tight. When fuel goes up with nowhere else to go, the all-in rate climbs with it. A sustained $10 increase in crude typically adds $0.20 to $0.25 per gallon at the pump, hitting directly at the operating margins of the 1.8 million trucking companies in this country, 90% of which are small businesses.

Fuel impacts in declining and tight markets

Fuel surcharges lag spot prices by a week or two, which means the increase hasn't fully landed in freight rates yet. It's coming. But the price signal alone still understates the risk. Geopolitical tension in the Middle East doesn't just raise energy costs, it reroutes the global supply chain. Ships bypassing the Suez Canal add thousands of miles to transit times. More miles, more fuel, more days, less efficient capacity utilization. The physics compounds the price. That's what ton-mile economics looks like when the map changes. The bigger question is whether demand holds long enough to absorb it. Watch volume.

Not everyone reads these signals the same way, and that's worth sitting with. Gad Levanon at the Burning Glass Institute rightly argues that GDP has been growing at 2.5 to 3.5 percent even as employment softened. When output grows while hiring slows, that's productivity growth, not recession. The US is also a net oil exporter now, meaning higher crude prices hurt consumers at the pump but boost the energy sector, making the net damage far smaller than what Europe or East Asia absorbs. The Chicago Fed's latest labor market data adds nuance too. What looks like a weakening jobs picture is actually a stasis: unemployment has risen about a percentage point since early 2023, but nearly 80% of that increase comes from lower job finding, not rising layoffs. Separations remain historically subdued. That's not the signature of a contracting economy. It's a tight labor market that stopped expanding. The freight bull case and the macro resilience case aren't necessarily in conflict. The question is whether the external shocks now building are large enough to overwhelm fundamentals that are otherwise intact.

The pattern that concerns me isn't unique to freight. History has a name for what happens when any system — political, institutional, economic — begins maintaining a gap between declared reality and actual reality because too many participants have staked too much on the narrative holding. Napoleon didn't consolidate power through ideology alone. He surrounded himself with accomplices whose advancement depended on affirming his judgment, dismantling the feedback loops that might have checked him. Political scientists call this Bonapartism: authority consolidating by positioning itself as the direct embodiment of popular will, making deliberative institutions seem not just slow but illegitimate. Experts become obstacles. Coordination becomes disloyalty. The gap between declared reality and actual reality becomes load-bearing, and when it collapses it collapses fast. The carrier that sits for days asking for rates it can't get. The market that keeps pricing in a soft landing it can't guarantee. The institution that keeps announcing stability it can no longer deliver. Systems built on narrative eventually collide with constraints that narrative cannot move. Logistics, physics, balance sheets.

What keeps most people from saying this out loud isn't agreement with the direction. It's something psychologists call pluralistic ignorance. Each person privately holds the concern but assumes they're in the minority because nobody around them is voicing it. The professional norm says don't mix business commentary with this kind of observation. So the signal stays suppressed. Everyone assumes the discomfort is theirs alone. It isn't. The institutional defense you're watching isn't mostly conviction. It's a collective action problem. Nobody wants to be the first one off the ship alone. But defection, when it begins, cascades for the same reason it stalled. Add alarm fatigue on top of that. Sustained threat signals stop being processed not because they're resolved but because processing them is exhausting. What looks like acceptance is really just drift with a calm face on it. That is not the same thing as stability.

This is where freight and the broader economy are running the same play at different scales. The status quo in freight for four years was: the downcycle is just the cycle, wait it out, don't reprice, don't invest. That position held until it didn't, and when it broke it broke fast. The status quo in equities and macro right now looks similar. Markets have been propped by AI concentration and the belief that policy chaos will work itself out, the same way shippers held out for gradual rate relief that never came. The deferred repricing doesn't disappear. It accumulates. The longer the gap between declared stability and actual risk conditions persists, the more violent the eventual adjustment tends to be.

The freight bull case is intact. Four years of carrier attrition, a rising cost floor, demand returning broad-based. What sits on top of those fundamentals now are shocks that aren't fully priced in: the diesel record, Hormuz disruption, potential CDL legislation that could deliver a structural capacity shock. None of them have fully triggered. The cycle can still run. The question worth asking right now is whether you're planning for optionality or betting that this one blows over too.

Institutions work when experts coordinate through them. Freight markets work when pricing signals are honest and participants act on them. Economies work when the people who see the risk are willing to say so, not from the rooftops, not in panic, but clearly, with the evidence in hand. The status quo is not a strategy. It is what happens to you while you're waiting for someone else to go first.